2026.03.09

15 billion paid in electronics tax

The Swedish Tax Agency has now calculated the 2025 tax revenue from the electronics tax, which is levied on all white goods, vacuum cleaners, PCs, mobile phones, screens, TVs and other home electronics. Since the introduction of the tax in July 2017, just over 15 billion (!) SEK has been paid to the Swedish Tax Agency by Swedish consumers, property companies, schools etc. in the form of significantly higher prices on e.g. laptops, TVs, mobile phones, washing machines and stoves etc.

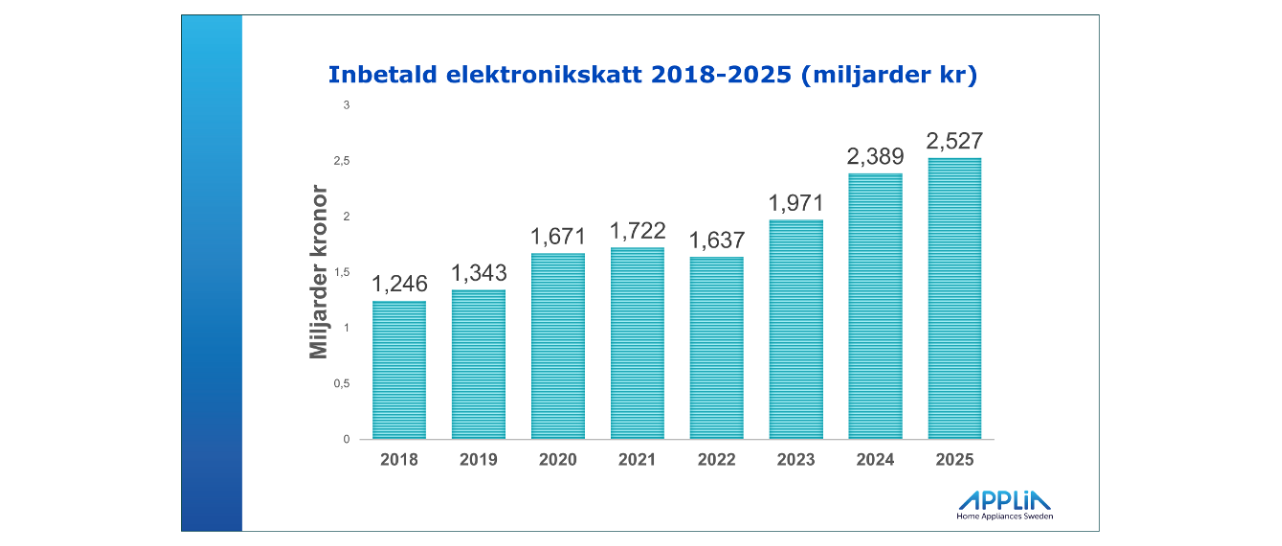

By 2025 – just over 2.5 billion in electronics tax

Despite a weak market development for white goods and home electronics during the year, the tax levy for the electronics tax (LSKE – the Act on Tax on Chemicals in Certain Electronics) will increase to a new record level of just over SEK 2.5 billion in 2025. The tax is levied per product sold and is charged according to the total weight of the product – not specifically the flame retardant chemical content. Even if the product were completely free of the relevant flame retardant substances, tax is still levied per product.

This year's tax outcome of SEK 2.5 billion also means that the annual tax collection has doubled since its introduction. A 100 percent increase must be some kind of record in the excise tax area, right?

It may be appropriate to remind you that the objective for the introduction of this Swedish special taxation was to reduce the presence of, among other things, certain flame retardants in electronics in homes. This objective is not even close to being achieved as the production of electronics and electronic components is for a global market. Furthermore, there are no bans on these substances and within the EU they are permitted via ECHA, which is the European Chemicals Agency.

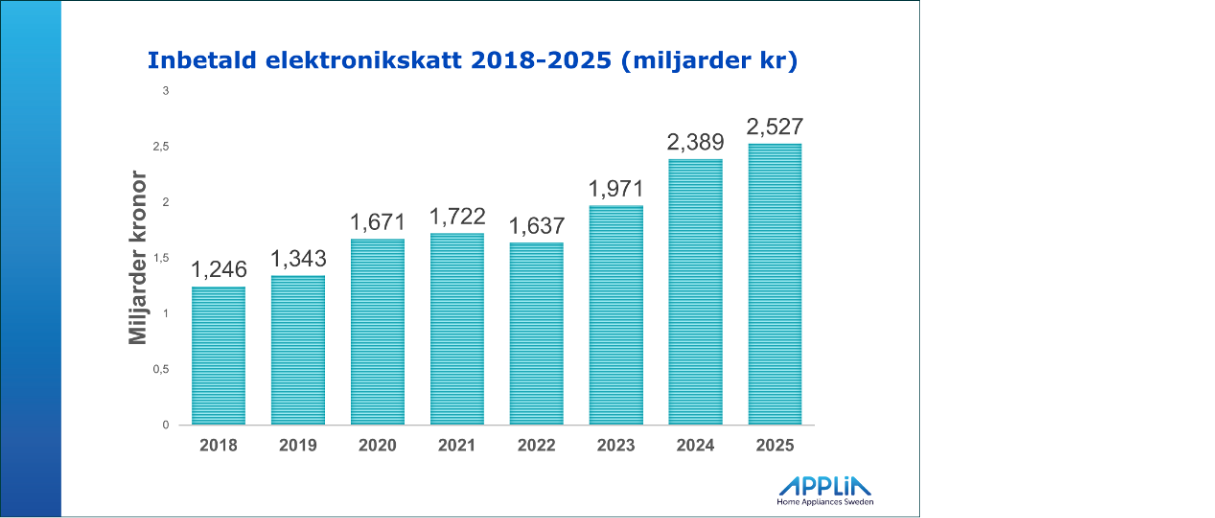

Which actors pay electronics tax?

Swedish producers, importers and Swedish trade, which constitute the majority of the so-called approved warehouse keepers, are the largest group of tax actors (493). In addition, the Swedish Tax and Customs Administration also categorizes smaller recipients (registered recipients), primarily private individuals (taxable by event) and the group of registered EU traders. This last group is e-tailers located within the EU and who have reported sales to Swedish customers. These constitute 7 percent of all tax actors that the Swedish Tax Agency keeps track of.

Which actors do not pay?

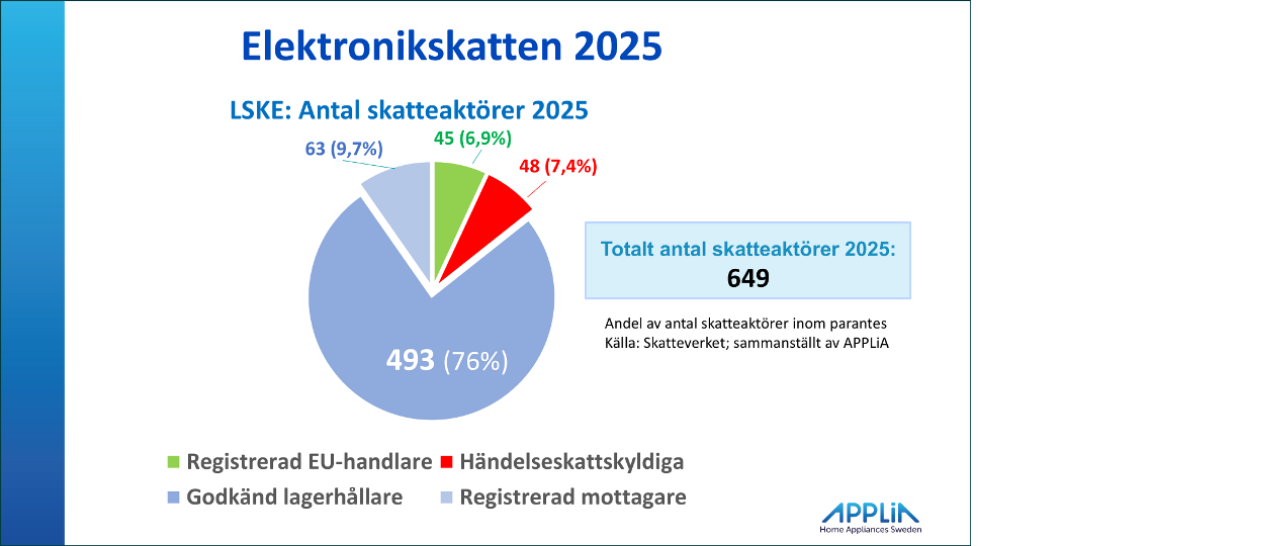

In the category of ”EU traders” there is reason to doubt the willingness to pay for the electronics tax. Only 0.7 percent of tax revenue comes from these. This is quite inconsistent with what we can read in the latest e-commerce barometer*) from Postnord, which shows that e-commerce from abroad is increasing sharply and that almost 18 million items have arrived at customers in Sweden in 2025. Almost half of all consumers in Sweden state that they have shopped online from a foreign online store in the past year. Mainly from China, but also strong trade from Germany, Denmark and the UK.

The category that is definitely missing among taxpayers is the sales that take place from non-European e-tailers and via rapidly growing trading platforms. For such imports, the private individual or company that is the recipient is responsible for declaring the tax, but here the control is obviously almost non-existent. This means that Swedish trade is exposed to unhealthy competition as the tax burden makes the goods in question up to 680 kronor more expensive (electronics tax + VAT on that tax) in Swedish trade compared to those who can avoid the tax. For Swedish physical and digital trade, this leads to the loss of many jobs.

//Kent Oderud

*) E-barometer – insights and trends in e-commerce | PostNord