2026.03.04

APPLiA Market for White Goods and Home Appliances 2025 – Annual Summary

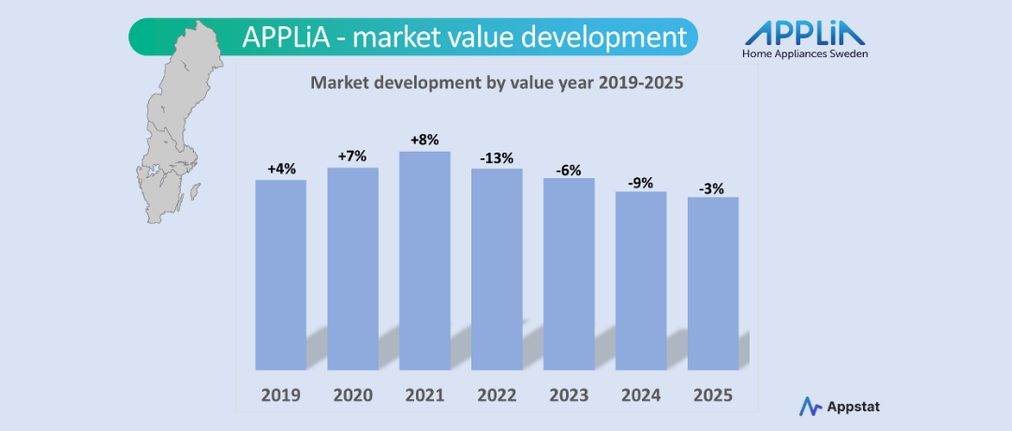

Marketing year 2025

In 2025, the white goods and household appliance industry in Sweden continued to be challenged by a weak economy, cautious consumers and low housing production, which meant that the market did not reach the previous year's level in terms of value.

Despite some recovery during the year and increased activity during the autumn, the APPLiA market's sales (sell-in value) after the four quarters reached a level that was 3 percent below the 2024 outcome. The "hyped" rise of the pandemic years resulted in a market saturation, which is persisting and is now causing subsequent years to suffer for it.

The development of the overall APPLiA market in 2025 can be described by the following market-influencing factors:

- Slow recovery: After a couple of tough years, the beginning of 2025 was marked by falling production, imports and consumption, and the recovery has been more protracted than previous forecasts indicated.

- Loss of value: The industry experienced a decline in value of over 3 percent compared to 2024, with smaller household appliances (SDA) in particular being hard hit, while larger appliances (MDA) fared somewhat better.

- Price development and costs: International trade tariffs and logistics challenges contributed to increased costs for appliances in 2025.

- Continued low level of housing construction: The number of completed and started homes is still at a comparatively low level in 2025 – although a trend reversal towards increased construction is discernible in the coming years.

- Extended RUT-deduction: The temporary increase in the RUT deduction until the end of 2025 resulted in a certain increase in, among other things, renovation of kitchens and laundry rooms, which provided marginal support for the recovery for larger white goods.

- Driving forces – Sustainability and technology: Despite the weak market, energy efficiency and smart technology (connected appliances) are clear drivers. Consumers are also prioritizing energy-efficient products that reduce energy consumption.

- Electronics tax: The Swedish special taxation on white goods, vacuum cleaners and home electronics of up to SEK 685 per product makes the products more expensive and gives foreign players a competitive advantage over Swedish trade. The tax collection in 2025 amounted to SEK 2.5 billion.

In summary, 2025 was a year of continued transformation where sustainability and technology were in focus, but where the high inflation and interest rate situation from previous years left a clear mark on consumers' wallets.

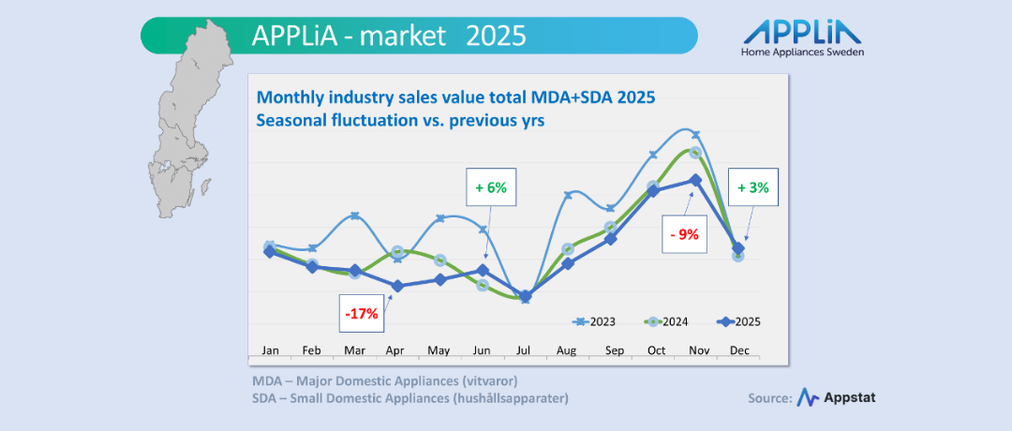

Market development during the year 2025

During the year 2025, market development follows the pattern that is clear throughout all years in this industry – the autumn months from August to November are the strongest in terms of turnover (see diagram above). In comparison to 2024, it is the development during the months of April/May and November that pulls down the annual outcome for companies in the industry, while at the beginning of the year, steady progress was maintained towards 2024. The months of June and December were even clearly better than the corresponding months in the previous year.

Compared to 2023, however, the comparison is significantly more negative, as can be seen from the diagram above.

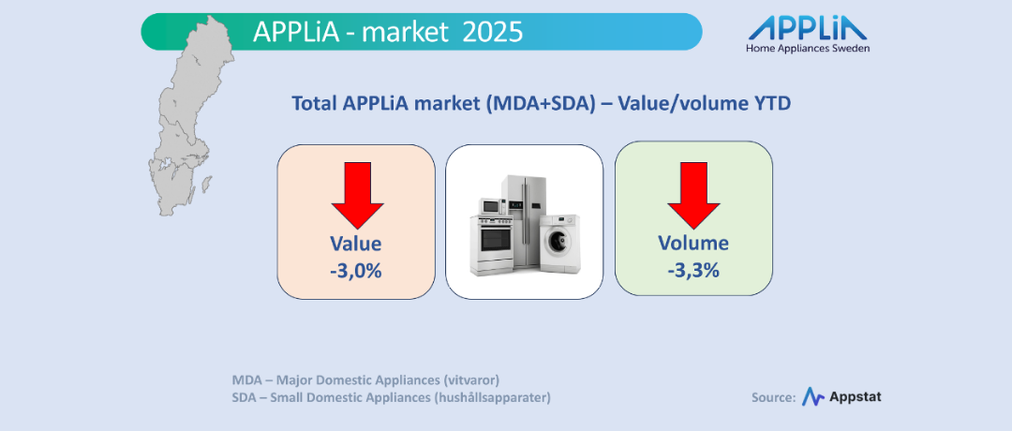

Reduced volume

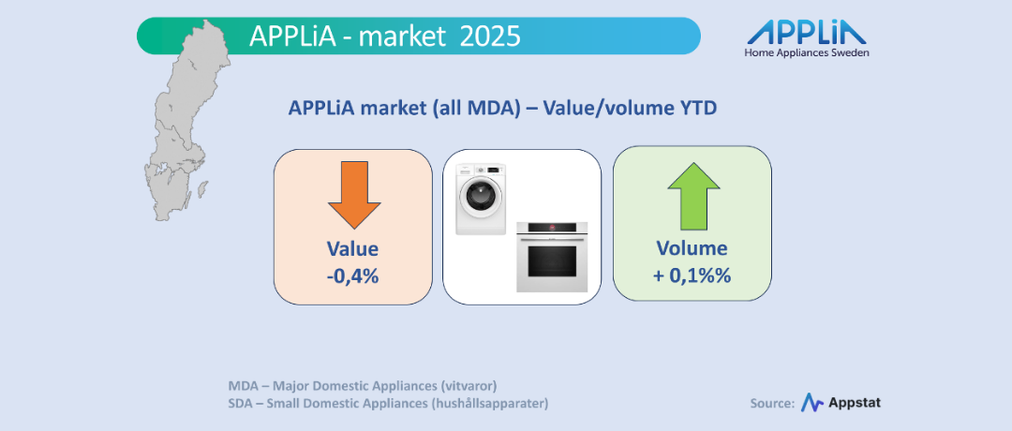

This year's value development of minus 3 percent corresponds to a volume decline of 3.3 percent in 2025 compared to the previous year across all product segments - both white goods and smaller household appliances. However, a certain difference is visible between the main segments MDA and SDA, where the larger white goods are leading the way and even show a marginal increase in volume.

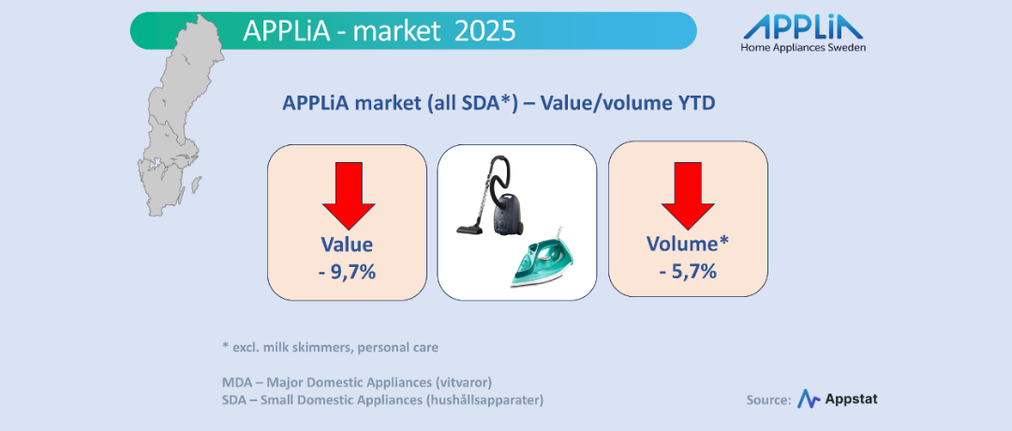

Tough year for household appliances

Domestic appliances (DSA) showed a volume decline of just under 6 percent, while sell-in value dropped by a whopping 9.7 percent. This also indicates a shift in the product mix towards lower-priced products and thus reduced average prices for these goods.

White goods on par with last year

Major appliances (MDA) have held up better than smaller household appliances and actually show a volume increase (albeit minimally by plus 0.1 percent) while the value decreases slightly. MDA has thus managed 2025 on a par with the previous year and has been helped by a more sustained sales growth in the latter part of the year.

To some extent, the expanded RUT deduction for work including renovation of kitchens and laundry rooms, lower interest rates and a generally improved consumption situation for durable goods have alleviated the situation somewhat.

In addition, consumers are increasingly looking for appliances that help reduce energy consumption, lower electricity bills and contribute to sustainability.

Kitchen hoods increase compared to last year

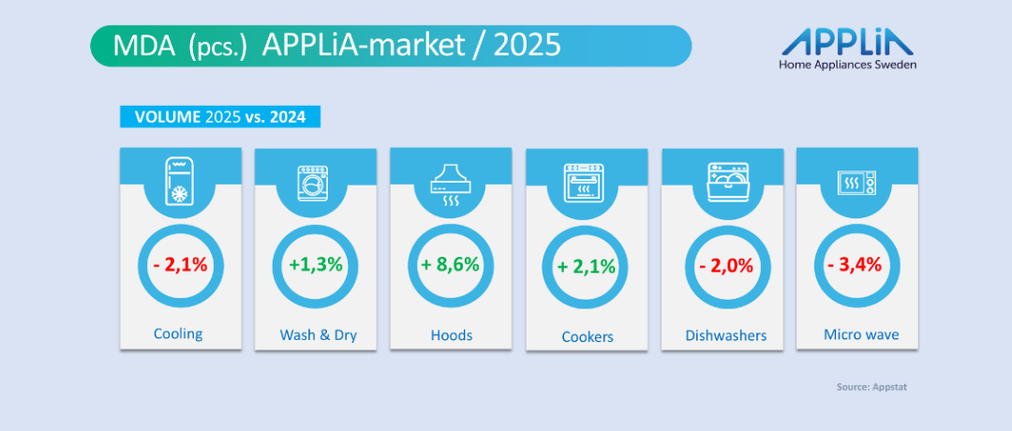

Within MDA, a volume development with both positive and negative figures for 2025 (see below) is reported for the various product areas. One area that stands out is kitchen hoods, which increase by 8.6 percent.

For this product area, it is the built-in and pull-out cooker hoods that account for the larger volumes. We can also note a big step forward for the fans that are integrated into hobs during the year. However, these volumes are reported under ”cookers” above.

Dishwashers are seeing a total decline in volume by 2 percent. This shows a clear increase in the share of integrated dishwashers (manufactured to be fitted with a carpentry door) to almost 30 percent from 27 percent in 2024. The opposite is seen in the ”narrower” dishwashers with a width of 45 cm, whose share decreases by a few decimal places to just over 8 percent of the total dishwasher volume.

”Cookers”, which include built-in ovens, stoves and hobs, will increase volumes by just over 2 percent in 2025. For the hob product area, the ”victory march” for hobs with induction technology continues – they now account for almost 80 percent of all built-in hobs sold in Sweden.

Within the washing and drying segment, it is clear that the larger washing machines (with a capacity of 8 kg and above) are increasing their volumes significantly at the expense of washing machines with lower capacities. Among dryers, the share of energy-efficient heat pump dryers is increasing significantly – from 77 percent in 2024 to 90 percent of all dryers sold.

The ”coolers” segment, which includes all products that provide cooling and freezing temperatures for food storage, is down a few percentage points (-2.1%). It is the large product areas of freestanding refrigerators, freezers and fridge/freezers that are not fully reaching the 2024 figures. Among the integrated refrigeration products, a smaller increase in volumes is reported for the year.

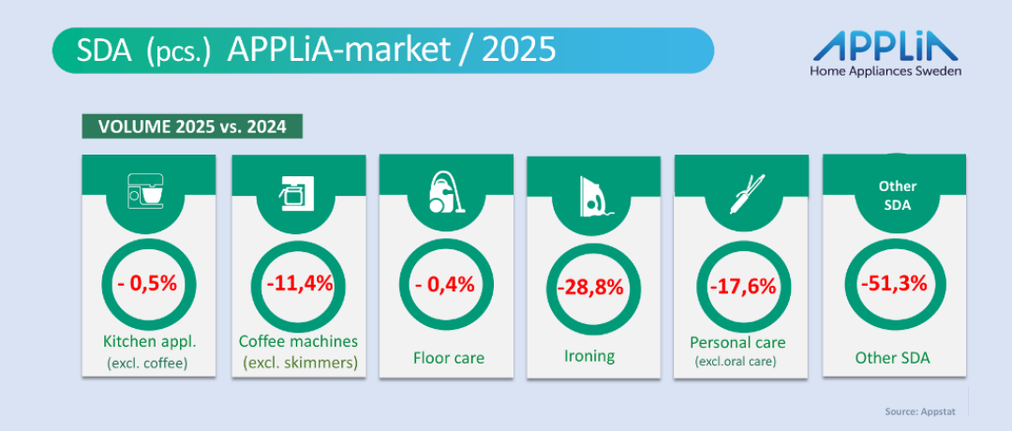

Household appliances (SDA) show red

Kitchen appliances (food processors, mixers, kettles, toasters, etc.) and vacuum cleaners are close to reaching last year's level in terms of volume, but by a few decimal places they fall short.

Coffee machines, which experienced a real boost during the pandemic with well over 1.2 million units sold in 2020/2021, now have no chance of meeting these levels and the volume in 2025 also landed well below last year (-11.4%). The market is fairly saturated with these pandemic volumes standing in Swedish homes and home offices.

”Ironing is mainly losing volume on the cheaper steam nozzles, so-called steamers, which have previously been a product that was sold in larger volumes seasonally during Black Week and in the Christmas shopping season. In 2025, this has happened to a lesser extent than before.

For "personal care", Appstat has had to clear some figures in last year's report for "oral care" (toothbrushes), which makes the report of the comparison with last year somewhat uncertain and has therefore been excluded. Remaining in the report in this product group are "hair care" and shaving equipment.

”"Other SDA" is a collective category for other household appliances that are not reported separately under their own categories. This can include, for example, table fans, heating blankets, kitchen scales, etc.

Future prospects – forecasts for 2026

Although 2025 was challenging, a certain improvement in the economy is predicted in general, which could have a positive impact on the trade in home furnishings and white goods going forward. Both within the consumer market and for the larger construction and real estate companies.

The renowned forecasting company Grand View Research states that the total consumer value of industry sales for white goods and household appliances in Sweden in 2024 will be 3.2 billion USD, which would correspond to 29-30 billion Swedish kronor and include VAT and other fees/taxes (electronics tax). And is expected to grow at an annual growth rate of 4.6 % between 2026 and 2030 according to the American research company.

Realistic-cautious forecast

When we have listened to our member companies, they are a little more conservative regarding a forecast for the full year 2026 and still end up with a somewhat recovered market development of around plus 3 percent in value terms. The lessons from the difficulties in achieving the forecasts in recent years nevertheless show that such a forecast should be enjoyed with a certain amount of caution.

Strong technology development

The forecast is supported by technological advancements that play a significant role in the market growth. Innovations in connectivity, artificial intelligence, and automation are transforming home appliances into highly efficient, user-friendly, and energy-efficient devices. Features such as voice control, integration with smart home systems, and advanced cooking or cleaning capabilities are attracting tech-savvy consumers. As manufacturers continue to invest in research and development, new product launches with groundbreaking features and energy efficiency will further stimulate market demand.

Compiled

//Kent Oderud