2026.04.20

March – a positive market month

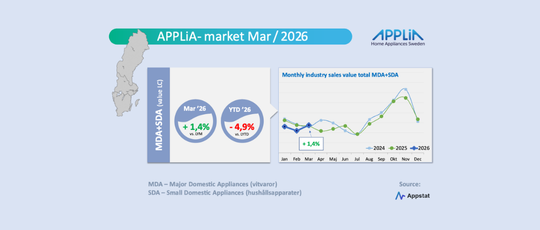

Finally a month with positive comparative figures compared to March of the previous year for the APPLiA market. Although this did not help quarterly results above the break-even point, it is still gratefully noted by the industry after a long series of negative market figures.

Weak development in quarter 1

March's "green" numbers above in the graph provided some much-needed oxygen to the industry, but still could not help the figures for the first quarter of the year to reach last year's. The industry's value development is now almost identical to what the first quarter of two years ago (2024) looked like, but is still well behind the relatively strong first quarter of last year (2025). Now the outcome within the APPLiA group is 4.9 percent below the first quarter of the previous year in value. And if we go back and compare with the year 2023 (not in the graph above), this year's value quarterly figure is clearly lower, by a full 16 percent in comparison. In the new figures, we can possibly read a stabilization of the market at a low level, but not yet any substantial turn of the market development in a positive direction overall.

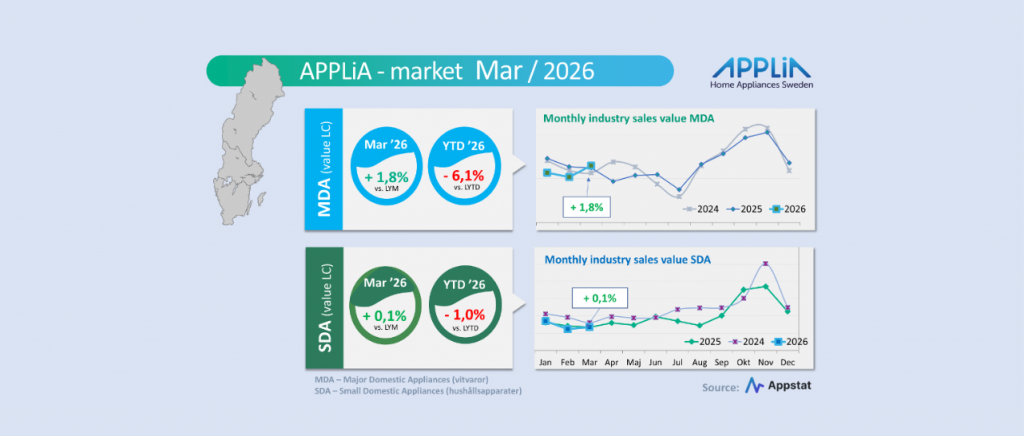

March showed positive numbers for both main segments

Both white goods (MDA) and small household appliances (SDA) had a slightly positive individual month compared to March 2025. In value terms, with plus 1.8 and plus 0.1 percent respectively. However, the quarterly results "Year-to-date" are still brilliantly "red". However, especially positive in the month within MDA, both "cooling" and "dishwasher" showed a pleasing positive development. Within the SDA segment, both coffee machines and larger kitchen appliances/assistants excelled positively during March. But the best month was "fabric care", which includes all ironing equipment for household use, where the monthly comparison gave a substantial plus compared to March 2025.

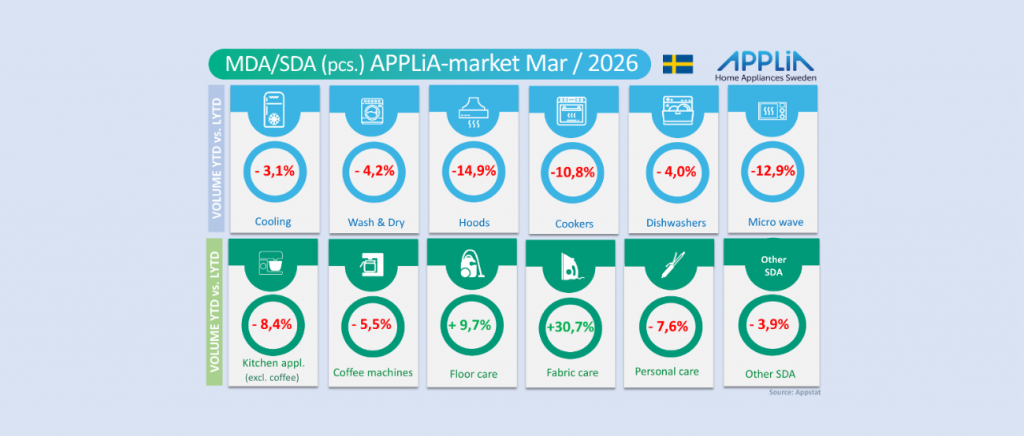

Volume development in the first quarter has "potential for improvement"”

The first quarter's volume outcome improved somewhat from the positive month of March, which we have left behind. However, volumes still generally have a long way to go to approach last year's level. For MDA in total, 7.1 percent of the volume is missing from the first quarter of the previous year. The corresponding figure for the entire SDA segment is 2 percent.

Nevertheless, we see some positive elements in the results after the first quarter of this year: Thumbs up for the categories vacuum cleaners (floor care) and ironing equipment (fabric care) which have managed to reverse the downward trend in volume to a clear increase. These increases are based on an increasing volume in so-called cylinder vacuum cleaners – both with and without bags – and on the traditional steam irons. Keep up the good work!

//Kent Oderud