Electronics tax

APPLiA, together with other industry associations, is conducting intensive advocacy work regarding the current Electronics Tax (LSKE), also called the Chemicals Tax. Here you will find current material in the debate.

Our policy

- Unilateral national taxation is not the right method to speed up the substitution of the current flame retardants as products with electronic content are standardized for sale in all EU countries. The EU's RoHS directive should instead be used as a tool for this to be effective.

- Swedish companies operate in a global market – The electronics tax de facto provides a substantial competitive advantage for foreign players, who sell to Swedish consumers to an increasing extent – as these are completely exempt from chemicals tax, which in the long run reduces tax revenues and the number of jobs in Sweden, without benefiting the environment since the imported products still contain the chemicals.

- The administrative burden of the electronics tax is unreasonable for companies and difficult to control by the authorities – there are still no testing methods to check the content of the products, which makes it difficult for all parties involved to ensure that the correct tax is paid and that competition is not being undermined.

- The design of the electronics tax – collection for the total weight of the product / without regard to the amount of the substances contained – makes the tax unevenly and unfairly distributed between industries.

- APPLiA is pursuing the issue of changes to the Electronics Tax and inclusion in RoHS for brominated flame retardants in consultation with the Confederation of Swedish Enterprise, the Swedish Technology Companies and the Swedish Trade Association.

Read more

More news about the electronics tax >>

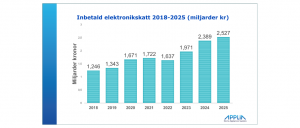

15 billion paid in electronics tax

The Swedish Tax Agency has now calculated the 2025 tax revenue from the electronics tax, which is levied on all white goods, vacuum cleaners, PCs, mobile phones, screens, TVs and other home electronics. Since the introduction of the tax in July 2017, just over 15 billion (!) SEK has been paid to the Swedish Tax Agency by Swedish consumers, real estate companies, schools, etc. in the form of significantly higher prices for e.g. […]

Increased electronics tax from January 1, 2026

The Swedish Tax Agency has now announced the new tax rates from 1 January 2026 for the Swedish electronics tax (LSKE) on white goods and home electronics. The index increase that takes place on this date normally follows the index from July to July. However, the 2026 index appears to have been at a slightly lower level than previously and ends up at an increase […]

New US tariffs hit European appliance and electronics industry hard

The US has imposed new tariffs of up to 50% on products containing steel and aluminium, now including white goods and consumer electronics such as washing machines, refrigerators and ovens. This is part of the US government’s ”national security strategy”, but in practice it means major cost increases for European exporters and the risk of reduced sales on […]

Roundtable discussion on the electronics tax

October's roundtable discussion on the electronics tax was held at the end of October at APPLiA with the participation of politicians and industry representatives. – We are pleased to be able to gather participants from both industry organizations, companies and politicians to discuss the unsustainable electronics tax. The goal is to discuss how we can work together to abolish the electronics tax and instead drive […]

”"The government was supposed to remove the electronics tax – but raised it even though it benefits Temu and Shein"”

APPLiA and the Electronics Industry in Current Sustainability: On September 22, the government will present its last budget for the mandate period. It is a last chance for the government to abolish the harmful electronics tax on white goods and home electronics that has no environmental benefit. This is written by Kent Oderud, chairman of the white goods industry's trade association Applia, and Pernilla Enebrink, CEO of the Electronics Industry. "Plastic bag tax, flight tax, increased electronics tax, […]

The government's investment is insufficient - the electronics tax must be abolished

When the government last Friday presented its commitment to a clean environment and a non-toxic everyday life, the most important announcement was conspicuous by its absence: the abolition of the electronics tax. Instead, the Swedish Chemicals Agency will receive a limited supplement of SEK 25 million from 2026. The aim is to strengthen control of products with harmful chemicals, not least imported goods from platforms such as Temu […]

White goods are taxed extra in Sweden

What are modern white goods made of? This is a question that is asked – not least for recycling reasons and as pure consumer information, but also by the Swedish Tax Agency. Since 2017, white goods have been taxed extra in Sweden with the so-called electronics tax of over 12 SEK per kilo measured on the weight of the entire product. The dishwasher, which weighs around 45 […]

The electronics tax shows why Sweden is losing competitiveness

Debate: Applia and the Electronics Industry in the Althing. The green transition is highlighted as Sweden's future, but investments are paused and commitment is decreasing. Symbolic climate measures, such as the electronics tax, are slowing down development. This is written by Kent Oderud, Chairman of Applia and Pernilla Enebrink, CEO of the Electronics Industry. In practice, many of the reforms that have been launched have been characterized by a combination of high ambitions and ill-considered symbolic politics. […]

Swedish Chemicals Agency: "High levels of banned substances in imports"

The Swedish Chemicals Agency recently presented its inspection report on consumer electronics for the year 2024. In this inspection project of all kinds of consumer electronics, the Swedish Chemicals Agency has checked the chemical content and labeling of 177 different products. The analyses looked for substances that are restricted in the RoHS Directive, the REACH Regulation and the POPs Regulation. Dropshipping companies worst The Swedish Chemicals Agency found in this review that products that […]

Abolish the electronics tax, the Confederation of Swedish Enterprise suggests in a new report "A new chemicals policy for Sweden"”

The Confederation of Swedish Enterprise, which represents the business community in Sweden and brings together 60,000 companies and 48 industry and employer organizations, recently presented a proposal for a well-developed chemicals policy for Sweden. And we can read in the report that such a policy is needed. National strategies exist for other policy areas such as climate, life science, food. But for chemicals policy in Sweden, a […]